Home » Export Drawback » Foreign trade enterprise export tax refund (exemption) declaration: Preparation guide

Forforeign tradeexport enterprises, applying for export tax rebates (exemptions) is a complex and crucial process that requires a series of preparatory steps. Below are some key preparatory steps:

Complete export tax rebate (exemption) registration: Foreign trade enterprises must first complete export tax rebate (exemption) registration, which can be done via the electronic tax bureau or using specialized offlineExport Drawbackdeclaration software.

Complete tax rebate selection: Value-added tax (VAT) special invoices intended for export tax rebates must undergo tax rebate selection, and the invoice verification data must be synchronized to the declaration system.

Confirm revenue: If export goods meet the conditions for revenue recognition, they should be confirmed promptly. This is because enterprises must confirm sales revenue when applying for export tax rebates.

After the goods are loaded onto the ship, the shipping company will issue a bill of lading confirmation. The export agency company will confirm the bill of lading information with the customer to ensure its accuracy. Subsequently, the shipping company will issue the original bill of lading, and the export agency company will settle all relevant costs with the customer, and at the same time handle the customs verification form.A complete export agency agreement should be attached with:Materials: Three types of export enterprises (newly established export tax rebate/exemption registration enterprises are typically classified as such) must submit foreign exchange receipt materials when declaring the previous years customs declarations after the April VAT tax declaration period. In other words, if the export tax rebate declaration is overdue, it can only be submitted after foreign exchange receipts are obtained.

Match customs declarations and invoices: Based on the purchase and sale relationship of export goods, match the customsExport Clearancedeclarations with the purchased VAT special invoices one by one. The product names on the VAT special invoices must match those on the customs export declarations, and the units on the VAT special invoices must match at least one measurement unit on the customs export declarations.

Choose an export tax rebate declaration system: There are typically three methods for declaring export tax rebates: using offline declaration software, declaring online via the electronic tax bureau, or using the single-window export tax rebate module. For convenience, online declaration via the electronic tax bureau is recommended.

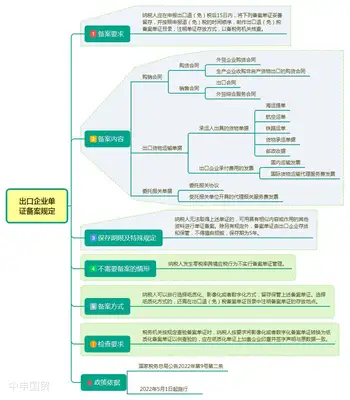

Manage export goods record-keeping documents: Within 15 days of declaring export tax rebates (exemptions), relevant documents such as purchase and sales contracts, export goods transport documents, and entrusted customs declaration documents must be filed in the Export Goods Record-Keeping Document Directory in the order of export goods, with the document storage location noted. In practice, it is advisable to collect and file these materials before declaring export tax rebates.

The above are some key preparatory steps for foreign trade enterprises applying for export tax rebates (exemptions). After completing these steps, enterprises can begin applying for export tax rebates.

Tags: Export Drawback

Related Recommendations

? 2025. All Rights Reserved. 滬ICP備2023007705號(hào)-2  PSB Record: Shanghai No.31011502009912

PSB Record: Shanghai No.31011502009912